Development charges (DC), also known as impact fees in some jurisdictions, are a one-time, upfront fee municipalities may charge paid for by developers for each new unit they build. Residential housing units are typically charged on a per-dwelling unit basis, while non-residential developments are charged a fee per square foot of gross floor area.

The council of a municipality may by by-law impose development charges against land to pay for increased capital costs required because of increased needs for services arising from development of the area to which the by-law applies. 1997, c. 27, s. 2 (1)

They are charged to cover the initial capital costs of expanding the capital infrastructure (roads, water, sewers, etc.) to provide these services to new developments and were initially implemented to combat NIMBYism:

Development charges evolved from post-1945 subdivision agreements and were initially accepted by most developers as a mechanism for enhancing the likelihood that current residents in a municipality would agree to new development. They now add as much as $90,000 to the cost of a new house in some parts of the Greater Toronto Area.

In 2017, 197 out of 444 municipal governments collected about $2.3B in DC revenue, while collecting approximately $21B in property tax.

It is one of 3 optional charges that municipalities can charge on development, the others are:

Community Benefit Charges

Cash-in-lieu of Parkland

“Growth pays for growth”

Growth (new homes, stores and other buildings) often requires the extension or expansion of municipal services (water lines, transit, but also police, transit and childcare) and DCs are the primary revenue tool municipalities in Ontario use to pay for these projects.

“Growth pays for growth” is a slogan often repeated by municipal members of council in Ontario and used to justify DCs. It is a guiding principle indicating an intent to make buyers of new homes pay for the cost of expanding municipal services to their location, rather than making existing homeowners (and voter base) pay for it through increased property taxes and user fees. It is related to the principle of “benefiter pays”, meaning infrastructure costs should be paid by those who will use and benefit from the installation of the services.

Critics have said it means “younger people pay for infrastructure upgrades” or “renters pay for growth“.

They are popular in municipal politics because they can be presented as a substitute for increasing property taxes – a strong incentive.

The philosophy behind them, logically speaking, is reasonable. New housing developments should pay the “true” price of the costs that they inflict on society in terms of infrastructure needs—roads, sewers, sidewalks, lighting, water, transit, parks, and so on—but also, perhaps, for municipal services such as policing, firefighting, public health, and schools.

While this is the slogan, in practice, growth-related costs aren’t necessarily 100% covered by DCs:

Since 1989 the DCA has been amended several times (1997, 2015), resulting in an overall lower level of cost recovery for municipalities. Growth-related costs have shifted from the development that created the costs to existing property tax and ratepayers.

According to a 2010 study by Watson & Associates: Long-term Fiscal Impact Assessment of Growth: 2011-2021 for the Town of Milton, after taking into consideration the various DC restrictions introduced in 1997, DCs only paid for approximately 80% of the cost of growth-related capital in Milton.

While a key principle is growth pays for growth consistent with the Province’s statements on the matter, GFTs have not fully covered the cost of growth in the past, nor are they expected to in the future. Legislative changes introduced through Bill 108 and 197 result in some positive changes to DCs; however, certain restrictions remain, such as the historical service level cap that does not allow for full recovery of growth-related costs. When growth does not pay for growth, the gap is funded by other funding sources, such as increases in property tax to support debt funding or addressed by reducing the level of services.

Ontario’s Housing Task Force recommends waiving DCs for infill affordable housing

Waive development charges and parkland cash-in-lieu and charge only modest connection fees for all infill residential projects up to 10 units or for any development where no new material infrastructure will be required.

Waive development charges on all forms of affordable housing guaranteed to be affordable for 40 years.

How DC increases are contributing to the housing shortage

Here is a great summary of the impact of government taxes on housing development across Canada:

What can DCs be used to pay for?

DCs received by a municipality must be placed into separate reserve funds for each service and may only be used for the purpose for which they are collected.

Services that municipalities may cover the cost of expansion for using DCs include:

What services can be charged for

(4) A development charge by-law may impose development charges to pay for increased capital costs required because of increased needs for the following services only:

Water supply services, including distribution and treatment services.

Waste water services, including sewers and treatment services.

Storm water drainage and control services.

Services related to a highway as defined in subsection 1 (1) of the Municipal Act, 2001 or subsection 3 (1) of the City of Toronto Act, 2006, as the case may be.

Electrical power services.

Toronto-York subway extension, as defined in subsection 5.1 (1).

Yonge North subway extension, as defined in subsection 5.1.1 (1).

Transit services other than the Toronto-York subway extension and the Yonge North subway extension.

Waste diversion services.

Policing services.

Fire protection services.

Ambulance services.

Services provided by a board within the meaning of the Public Libraries Act.

Services related to long-term care.

Parks and recreation services, but not the acquisition of land for parks.

Services related to public health.

Child care and early years programs and services within the meaning of Part VI of the Child Care and Early Years Act, 2014 and any related services.

Repealed: 2022, c. 21, Sched. 3, s. 2 (2).

Services related to proceedings under the Provincial Offences Act, including by-law enforcement services and municipally administered court services.

Services related to emergency preparedness.

Services related to airports, but only in the Regional Municipality of Waterloo.

Additional services as prescribed. 2020, c. 18, Sched. 3, s. 1 (2); 2021, c. 34, Sched. 7, s. 1; 2022, c. 21, Sched. 3, s. 2 (2).

Some of it goes to housing-related infrastructure, while some goes to things like $144 million soccer facilities in Kitchener including a full FIFA-sized indoor turf soccer field, where over $100M came from DCs:

Worth noting is that Kitchener has higher DCs for suburbs than for infill development.

Municipalities must publish a statement on DC reserve funds annually on their website

Municipal services cannot be funded from DCs (i.e. cultural, tourism, cemeteries, general administration, etc.). Costs for those services must be paid from the tax base or other funding mechanisms.

A development charge by-law may not impose development charges with respect to local services described in clauses 59 (2) (a) and (b)

(a) local services, related to a plan of subdivision or within the area to which the plan relates, to be installed or paid for by the owner as a condition of approval under section 51 of the Planning Act;

(b) local services to be installed or paid for by the owner as a condition of approval under section 53 of the Planning Act. 1997, c. 27, s. 59 (2).

Sections 2 to 4 of the DCA outlines the exemptions of certain developments from DCs:

Section 2 to 4 of the DCA exempts the following:

Municipally-owned lands used for purpose of a municipality, local board, or board of education (eg. construction of schools by public or Catholic boards) – S. 3

Non-profit housing development – S. 4.2 (2)

Creation of residential units

Enlargement of an existing residential dwelling unit – S. 2 (3)

Adding 1 unit or 1% of existing residential units to existing apartment building – S. 2 (3.1)

In existing houses or new residential buildings – S. 2 (3.2 and 3.3):

Second residential unit in a detached house, semi-detached house or rowhouse

Third residential unit in a detached house, semi-detached house or rowhouse

One residential unit in a building or structure ancillary to an existing detached house, semi-detached house or rowhouse

Industrial expansion

Expansion of existing industrial building’s gross floor area (S. 4) by:

50% or less is fully exempt

50% or more is charged only on the portion exceeding the 50% threshold

Creation of affordable and attainable units

New residential unit intended to be an affordable for 25 years or more – S. 4.1 (8)

New residential unit intended to be an attainable when first sold – S. 4.1 (10)

Section 6.1 of O. Reg. 20/98 – Education DCs provides additional exemptions, including for universities in Ontario that receive operating funds from the Ontario government as per the Ministry of Training, Colleges and Universities Act.

Municipality exemption examples

Municipalities may set their own exemptions in the bylaw to incentivize/subsidize certain kinds of developments. Revenue shortfalls resulting from exemption policies cannot be recovered through fee increases for other types of development. The difference is made up by increasing property taxes and water/wastewater rates.

Commercial Core Sub-Area and the Waterfront Commercial Sub-Area of the Central Area, as depicted on Schedule J of the Official Plan of the City

Redevelopment in Central Area, as depicted on Schedule J of the Official Plan of the City, and which exists as of January 1, 2005

15+ apartment units in Central Area

Mixed-used development (15+ apartment units and 1,000 sqm of commercial floor area) in Central Area. Each additional 67 square metres of commercial gross floor area beyond the initial 1,000 square metres must be matched with a residential unit to be eligible for exemption.

50% for 6+ unit apartment buildings outside the Central Business District that agree to charge “affordable rents” (at or below market rate for County of Hastings) for a defined period of time

Provided deferrals (payment plans) for:

Rental housing (that is for-profit), and institutional development – Payable in 6 instalments beginning from the date of issuance of an occupancy permit or occupancy of the building, whichever is earlier.

Non-profit housing development. Payable in 21 instalments beginning from the date of issuance of an occupancy permit or occupancy of the building, whichever is earlier.

Developers that belong to the Quinte Home Builders Association – Contact the City at 613-968-6481 for details.

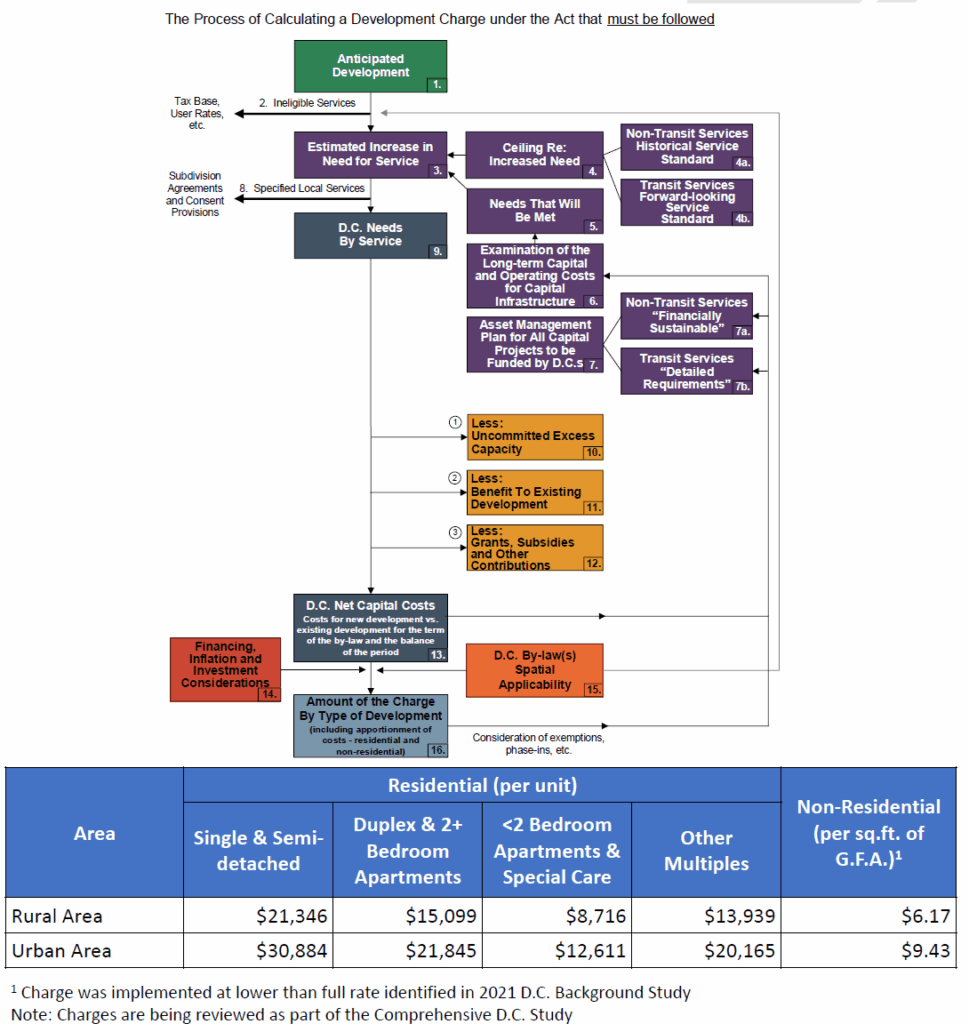

How are DCs determined in Ontario?

Municipalities must prepare a DC Background Study which informs the calculation of the DCs.

Before passing a development charge by-law, the council shall complete a development charge background study.

The study looks at the anticipated residential and non-residential growth over the next five years.

Section 10 and Section 5 of the DCA require the development charge background study to consider:

Forecast of the amount, type and location of development, for which DCs can be imposed

For each service to which the development charge by-law would relate, the

Increase in the need for service attributable to the anticipated development

Average historical level of service over the previous 10 years for each eligible service area (i.e. parks, recreation, roads, libraries, waste diversion, etc.). This historical level of service forms a cap that new cannot be exceeded through DCs.

Capital costs necessary to provide the increased services must be estimated, including:

Costs to acquire land or an interest in land, including a leasehold interest, except in relation to such services as are prescribed for the purposes of this paragraph.

Costs to improve land.

Costs to acquire, lease, construct or improve buildings and structures.

Costs to acquire, lease, construct or improve facilities

Interest on money borrowed to pay for costs described in paragraphs 1 to 4. 1997, c. 27, s. 5 (3); 2020, c. 18, Sched. 3, s. 2; 2022, c. 21, Sched. 3, s. 5 (3, 4).

Long term capital and operating costs for capital infrastructure required for the service

Consideration of the use of more than one development charge by-law to reflect different needs for services in different areas

Asset Management Plan

Rates vary by:

Municipality based on service levels, cost of living

Development type based on their expected need of different municipal services

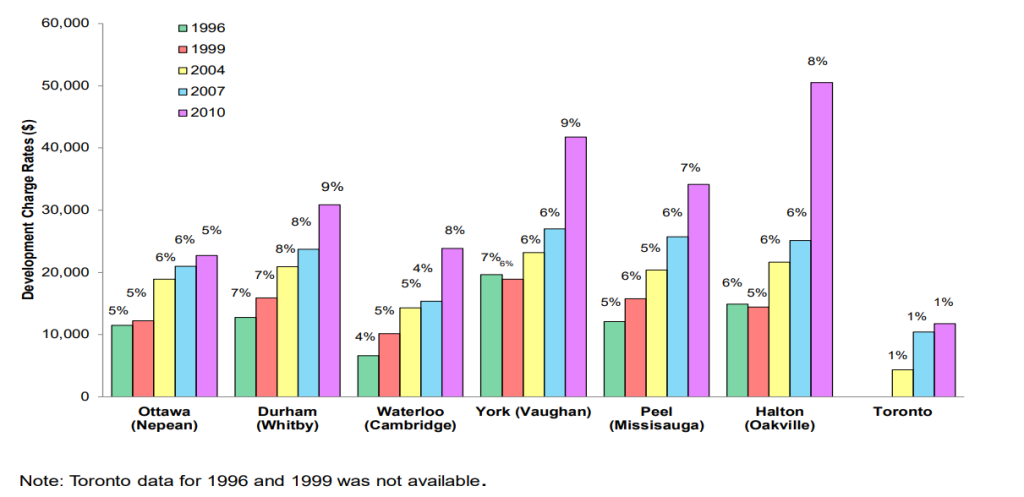

DCs are included in the cost of a new home and have represented between 5 to 7% of the cost of a new single-family home according to the Association of Municipalities Ontario, while the CMHC found them to be 2% to 13% in Toronto in 2022.

Historically, they’ve been around that proportion of the cost of a home in municipalities across Ontario:

Select municipalities, 1996 to 2010

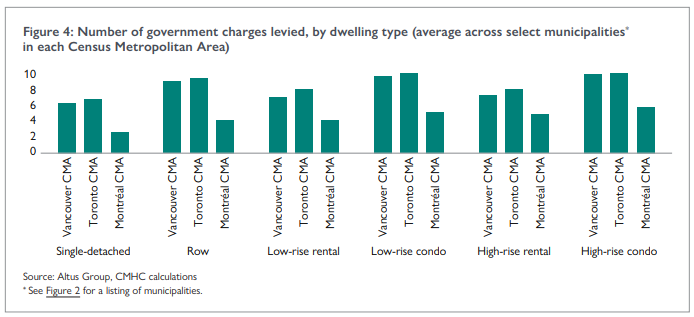

Development charges are only a portion of total government charges

They are only one of the fees on a home’s construction, with some municipalities having up to 10 different charges:

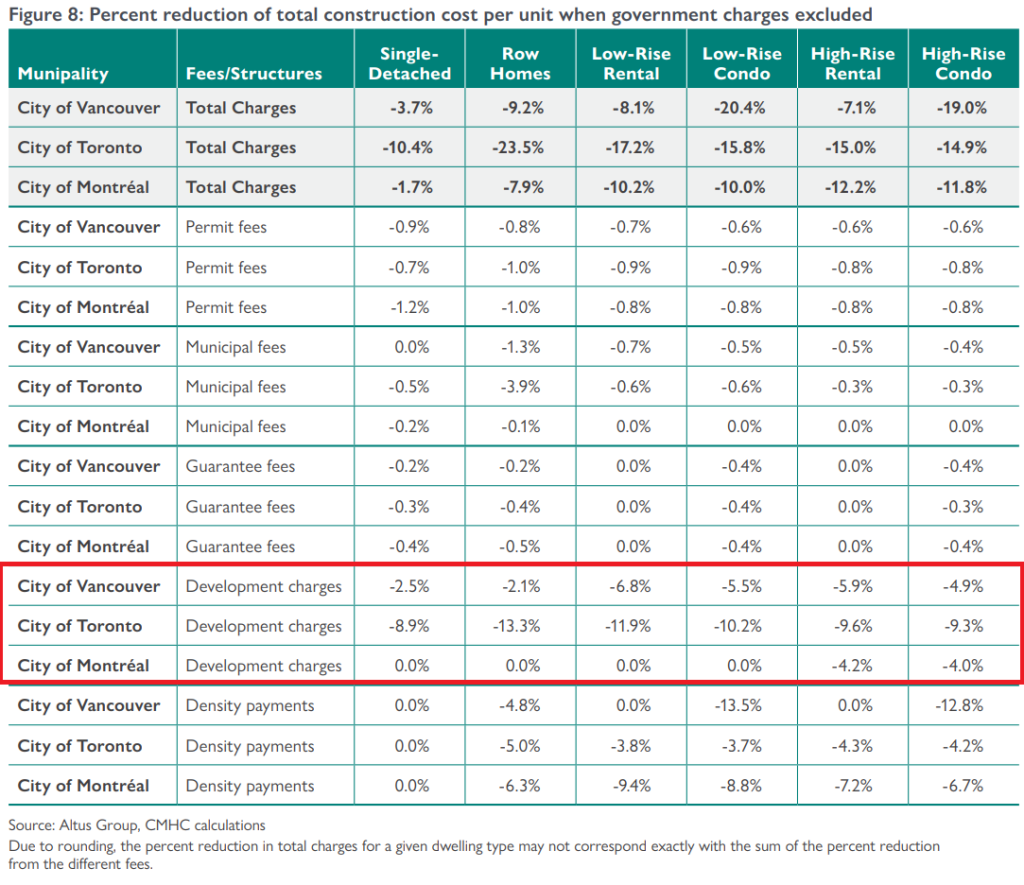

Total government charges can account for more than 20% of the construction costs of a dwelling unit in some major Canadian cities. Include sales taxes on the purchase of a new home (13% HST in Ontario – 5% federal and 8% provincial) and the portion the government’s portion can amount to 31% of the purchase price of a new home in Ontario, according to a report by the Canadian Centre for Economic Analysis on behalf of the Civil Construction Alliance of Ontario (RCCAO).

Charges for single detached units have increased much faster than inflation and construction prices over the last 20 years

Over a 20 year period between 2004 and 2024, an analysis of 27 municipalities in Ontario found that all of them increased their development charges for single detached units more than the rate of inflation in Canada (54%) and the increase the Non-residential Building Construction Price Index (144%), which many municipalities have since indexed their development charges to.

Some municipalities increased their charges by as much as 800%:

It does not include fees applied by regional municipalities and school boards or other fees such as Community Benefits Charges or Cash-in-lieu of Parkland.

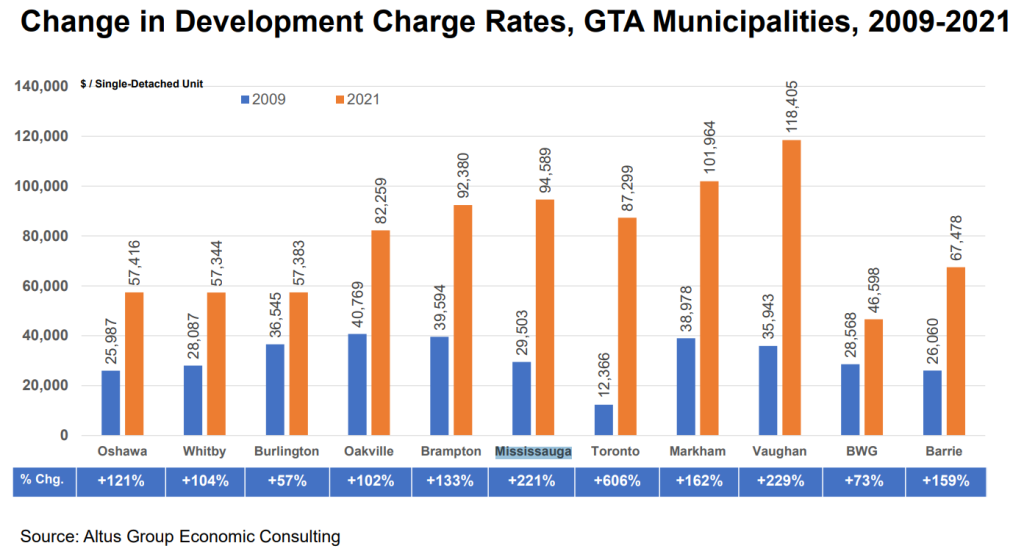

Here is the change from 2009 to 2021 according to a report prepared by Altus Group for BILD:

Housing prices in Ontario have increased 336% between January 2005 and March 2024 (average of 6.24% per year), while inflation increased around 50% in that same time period (2.18% per year on average):

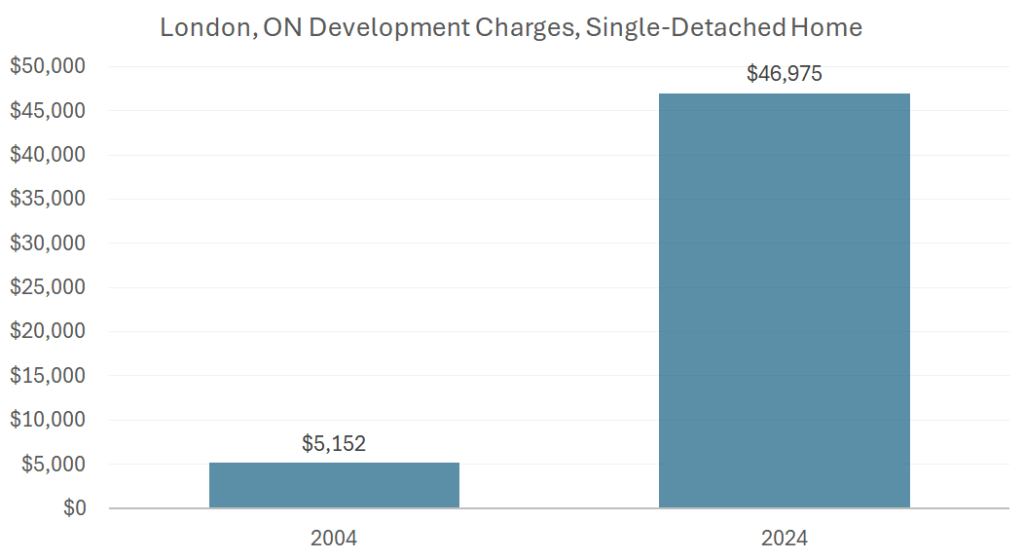

For example, in 2004 the development charges for a single-detached home in London, ON were $5,152. The charges would cost $7,932.87 if adjusting for the inflation of 53.8% between then and 2024 (2.18% per year on average). However, they’ve gone up over 800% in that same time period:

A detached home in London, ON which cost $168,000 in 2004, (~$250,000 adjusted for inflation) sold for $665,000 in September 2023 – a 266% increase. Interest rates are roughly the same now as they were then, so the price increase isn’t due of low interest rates (anecdotal example from this thread by Dr. Mike Moffatt). According to the Benchmark Price, prices have increased by 400%.

Regional Municipalities and school boards may also impose their own development charges

Education/school boards

Section 257.54 of the Ontario Education Act allows school boards to establish development charges on land undergoing residential and non-residential development. The school boards are responsible for setting and imposing education development charges (EDC). The revenue collected is used to purchase land for new schools and to pay for site preparation costs. The municipality is responsible for the collection of the education development charges on behalf of the local school boards at building permit issuance.

Regional Municipalities

The DCA allows municipalities, including regional municipalities to impose development charges to pay for increased capital costs required because of increased needs for services arising from development of the area to which the by-law applies.

For example, the Region of Durham’s Regional Residential and Non-residential Development Charges bylaw was passed on June 14, 2023, applying uniform development charges against all lands within the boundaries of the Region that are developed for residential and non-residential uses.

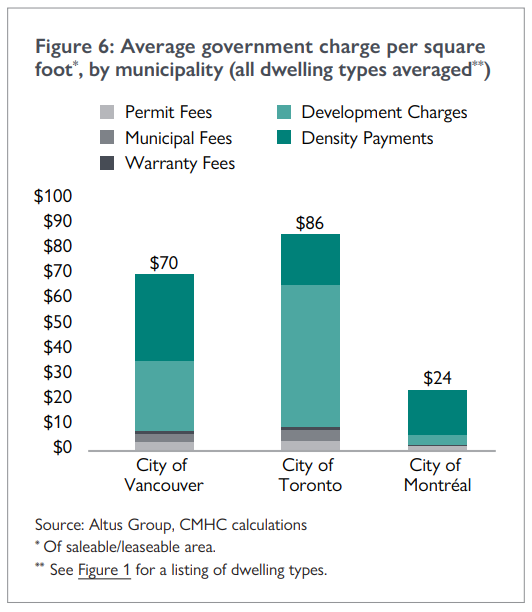

Charges on single detached homes are often lower than on apartments, incentivizing single detached homes

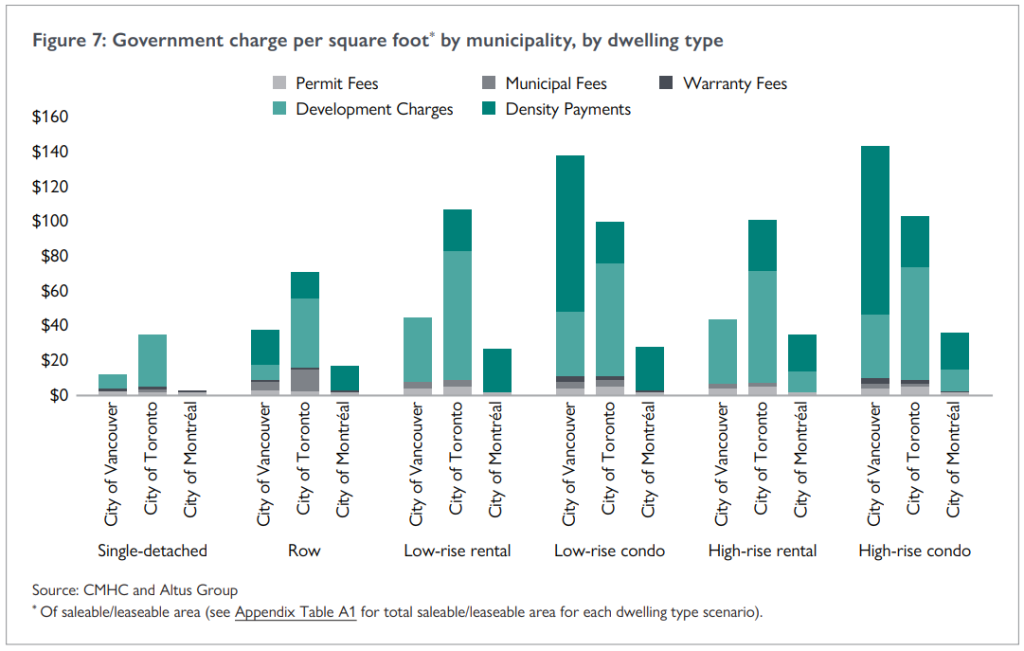

Government charges in Vancouver and Toronto for single-detached homes are much lower than for denser housing types such as row homes and condominiums. In a context in which many municipalities have implemented policies to increase density, it may seem surprising that the least dense housing type is also the one whose total cost is least affected by government charges:

Development charges might make more sense if higher fees were charged for suburban single family developments and lower/no fee was charged for dense apartments (to reflect the fact that low density is way more expensive than high density). However, single family homes are generally charged the lowest development fees per square foot while denser construction is charged higher fees.

However, that isn’t always the case. In 2013, to steer growth and encourage greater density, the City of Ottawa levied a lower development charge ($16,447 per Single Detached Unit) for development within the inner boundary of the city’s designated Greenbelt than areas beyond the outer boundary of the Greenbelt ($24,650 per Single Detached Unit) and still does in 2024, but by a smaller margin.

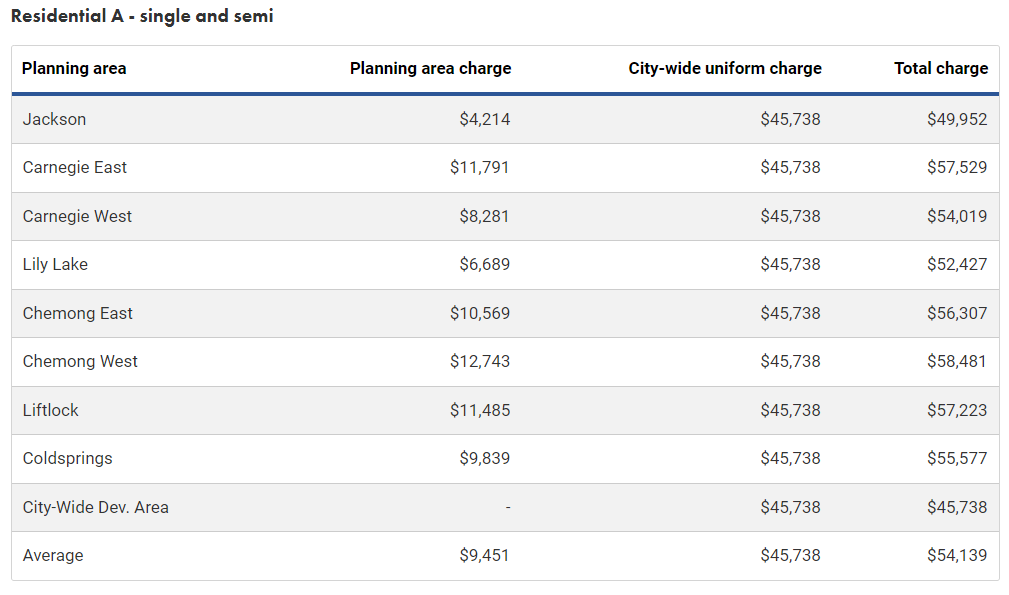

Approaches determining charges vary considerably between municipalities

Municipalities define different categories, including:

Areas

Greenfield/infill

Urban/rural

Named areas (eg. Chemong East)

Unit types: single detached, duplex/triplex, apartments, etc.

GTA charges higher than in other Canadian cities, US

A 2019 study for BILD showed that development charges in the Greater Toronto Area for low-rise housing are on average more than 3 times higher per unit than in 6 comparable US metropolitan areas, and roughly 1.75-times higher than in the other Canadian cities. For high-rise developments the average per unit charges in the GTA are roughly 50% higher than in the US areas, and roughly 30% higher than in the other Canadian urban areas.

Municipalities had $10.6B sitting in development charge reserves in 2022

As of December 2022, Ontario municipalities had $10.6B in their development according to analysis by Mike Moffatt using of the Financial Information Returns:

I’ve had a lot of questions in my feed on what development charges are allocated to. It’s mostly roads and water/wastewater infrastructure. Not schools.

As of Dec 2022, Ontario municipalities had $10.6 billion in unspent development charge reserves. pic.twitter.com/asGH8Ti3KR

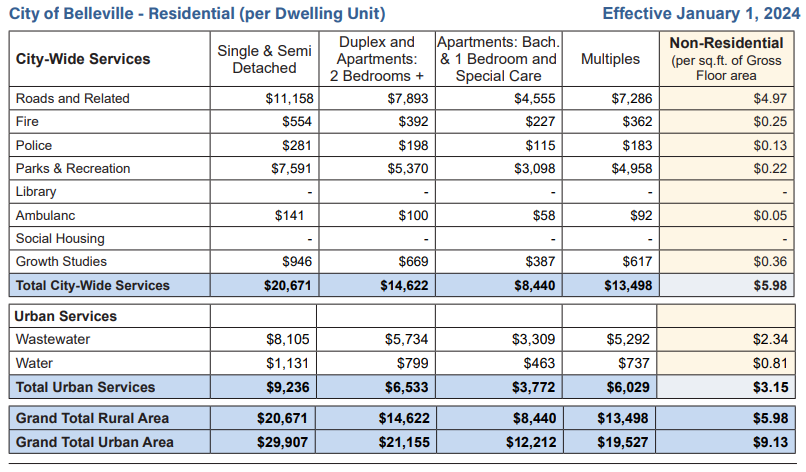

In Belleville, Development Charge deferrals available include:

Rental housing (that is for-profit), and institutional development. Payable in 6 instalments beginning from the date of issuance of an occupancy permit or occupancy of the building, whichever is earlier

Non-profit housing development. Payable in 21 instalments beginning from the date of issuance of an occupancy permit or occupancy of the building, whichever is earlier.

Developers that belong to the Quinte Home Builders Association. Contact the City at 613-968-6481 for details

The Montréal model

Montreal does not charge developers impact/development fees. Instead, growth-related infrastructure is still largely financed through municipal borrowing (long term debt) that is paid back by property taxes paid by all property-owners in the municipality. Quebec municipalities are some of the most indebted in Canada.

The city’s housing stock stands out in North America for its strong presence of row houses, duplexes, triplexes, and low-rise apartment blocks—what urbanists call elsewhere the “missing middle.” The middle is certainly missing in Toronto, its market skewed toward the two extremes: single, detached houses and high-rise apartment towers.

Montreal’s housing stock is visibly more affordable. The percentage of owner households spending more than 30 percent of their income on shelter costs was 20 percent in Montreal, compared with 27 percent in Toronto (16 percent and 27 percent, respectively, at the metro level). The equivalent figures for renters were 37 percent and 47 percent (city) and 36 percent and 47 percent (metro area).

Instead of charging new homebuyer’s, municipalities could take out long-term debt to pay for the expansion of services. Interest rates may fluctuate, but municipal rates are generally lower and more stable than the mortgage rates homeowners must pay to, in part, pay for the cost of development charges.

How using debt instead of development charges would impact Ontario municipalities

Halton Region had the highest development charges in 2020 and raised $258M. If the $258M was instead financed at 2.5% over 20 years, the average property tax increase would be 1.8%. Expanding the concept to the $2.23 billion collected by Ontario municipalities in 2018, the average property tax increase over the whole province would be 0.7%.

Interest rates can obviously go up or down, most likely up, given the current low rates. If the worry is the potential increase in municipal capital borrowing rates, we should have similar concerns about the exposure of new homebuyers to increased mortgage rates (which are higher than municipal borrowing rates) and monthly payments, a substantial portion of which often goes to paying the cost of development charges.

DCs received by a municipality must be placed into separate reserve funds for each service for which they are collected and may only be used for the purpose for which they are collected.

A municipality that has passed a development charge by-law shall establish a separate reserve fund for each service to which the development charge relates.

The municipality shall pay each development charge it collects into the reserve fund or funds to which the charge relates.

Section 34

The money in a reserve fund established for a service may be spent only for capital costs determined under paragraphs 2 to 7 of subsection 5 (1).

Section 35

In 2011, municipalities collected $1.3B in DCs and had $2.7B in obligatory reserves funds. In 2017, 197 out of 444 municipal governments collected about $2.3B in DC revenue and at the end of 2019, had $3.25B held in reserve funds. $839M of the increase was from increases in Toronto’s reserves.

Requirement to spend or allocate monies in water reserve funds

(2) Beginning in 2023 and in each calendar year thereafter, a municipality shall spend or allocate at least 60 per cent of the monies that are in a reserve fund for the following services at the beginning of the year:

1. Water supply services, including distribution and treatment services.

2. Waste water services, including sewers and treatment services.

3. Services related to a highway as defined in subsection 1 (1) of the Municipal Act, 2001 or subsection 3 (1) of the City of Toronto Act, 2006, as the case may be. 2022, c. 21, Sched. 3, s. 10.

Proponents of DCs

As a rule, urban planners, environmentalists, and municipal administrators favor [development charges] —the first two groups, historically wary of developers, because they see the fees as a means of controlling development; and the third group because the fees are a rich source of revenue.

Institute on Municipal Finance and Governance (IMFG)

New infrastructure like bridges, traffic lights, water lines typically indivisible – it is either built or it isn’t – and they often need to be built in advance, well before houses are constructed.

Since growth-related capital works create excess capacity upfront while growth generates revenue only after it materializes, the cost of these works is front-ended, whereas cost recovery from growth is back-ended. This timing mismatch means growth generates insufficient revenue over the growth horizon to recover corresponding growth-related capital costs, and the shortfall is shifted to existing ratepayers in the form of higher user fees and property taxes, causing:

Reduced service levels and growth: Existing ratepayers respond to inflated user fees and property taxes with demands to reduce municipal services below efficient levels. Reduced municipal services depress property values and discourage growth. Growth is depressed even further as municipalities respond by slowing or halting development approvals.

Diminished fiscal capacity: The shifting of growth-related capital costs to existing ratepayers imposes secondary inefficiencies on municipalities in the form of diminished fiscal capacity and an increased risk of debt regulation violations, credit downgrading, or even financial insolvency. These effects increase borrowing costs, further diminishing service levels and growth.

Increased service congestion: If a municipality tries to mitigate the nonconcurrence externality by investing in growth-related capital works after the associated growth occurs (which is feasible for services other than water and sewage systems), existing and new ratepayers experience increased service congestion. Although such congestion is a non-monetary cost, it is a cost nonetheless, and one largely borne by existing ratepayers.

No, these fees do not add to the price of a new home — the market determines housing prices. No, there is no guarantee that reducing these fees will make developers build more housing or make it more affordable – Bill 23 does not require them to. Yes, developers will still make a profit.

Development charges are not a root cause of the affordable housing and supply challenge in Ontario. Even further to the point, DCs only apply to only a small part of the housing market – new homes. DCs represent between 5 – 7% of the cost of a new home.

A reduction in development charge collections will increase the cost of public services for all residents. This will increase pressure from taxpayers to constrain growth and to constrain demands on the already stretched property tax dollar.

Municipal governments and current property taxpayers do not have means to subsidize developers in building new homes. Changes that reduced development charges has never resulted in reduced housing prices.

New development should pay for the growth-related infrastructure, services and facilities needed to support the new population and employment. Changes to provincial legislation should maintain municipal revenues – that is, the City should not be worse off as a result of the new legislative requirements.

Provincial legislation should consistently allow municipalities to recover the full cost of infrastructure related to development. As noted above, amendments to the DCA since 1989 have reduced municipalities’ overall ability to recover growth related costs. This means that existing taxpayers must pay the cost of infrastructure for new communities. The mechanisms to permit cost recovery should be efficient, as any accompanying administrative burden can result in slower provision of requisite infrastructure and services, thereby slowing housing development.

The establishment of house prices is primarily based on demand and supply conditions in the housing market, not by development costs. Demand arises from dynamics like population growth, local employment opportunities, transit and infrastructure investments, and neighbourhood amenities. Supply is determined by the characteristics of planned developments, as well as the characteristics and performance of resale homes in the secondary market.

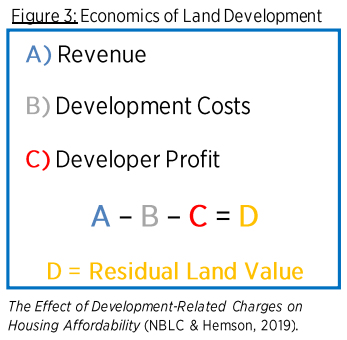

A developer’s decision to purchase or develop real estate is based on whether a project is ‘feasible’ or ‘viable’ from the developer’s perspective. Developers determine this by calculating the Residual Land Value (RLV) of a given project. The RLV lets the developer know how much they can pay for a potential parcel of land given their specific redevelopment plans.

Market pricing may drop due to demand and supply conditions. Development costs may rise due to general inflation or increased fees. A developer’s profit expectation may increase, based on other investment opportunities. Such changes to the inputs would reduce the RLV (the amount the developer is willing to pay for land) and could impact project viability. However, a change in development costs will not result in a change in the market price of the development, because these two parts of the equation are not dependent on each other.

The addition of new community amenities and infrastructure can improve the quality of life for existing residents as well as new ones. For example, Kitchener’s new multi-purpose indoor recreation facility. In addition, more population may mean more businesses and services too choose from (here in Belleville we’re still waiting for a Costco).

Proponents of the fees often fail to consider the potential benefits of growth experienced by all residents which “include growth in retail sales and sales tax collection, expanded employment opportunities, increased disposable income, and diversity in housing choices” (Bauman and Ethier, 1987: 51–52).

Proponents of the slogan “growth should pay for growth” are in support of this outcome because they believe that growth-related infrastructure costs can be fairly separated from other local infrastructure costs and that current residents have no moral responsibility for such costs. Much of this report has been devoted to showing the shortcomings of such a view.

Developers push for adjustments to how they are determined

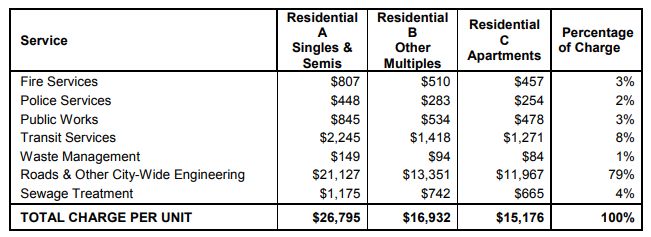

A study of 16 GTA municipalities by Altus Group on behalf of Building Industry and Land Development Association (BILD) found that:

Municipal charges for low-rise housing amount to $53 per square foot, while charges for high-rise housing amount to $99 per square foot – municipal charges are nearly 2-times higher for high-density housing. This relationship is evident in every municipality studied, with the ratio of high-rise charges ranging from 1.5 to 2.4-times the charges per square foot levied on low-rise development. These ratios would be even higher if the costs associated with inclusionary zoning were included, as that initiative is currently applied to high-density housing only

Higher municipal charges (like escalating construction costs or other costs) increase the price ‘floor’ that units need to be sold at to be feasible for the developing landowner or home builder. If fewer units can sell at prices that cover increased costs, fewer units will get built

This puts at risk municipal objectives for increased infill and intensification and could hinder utilization of public infrastructure investments in urbanized areas, such as major transit station areas, or transit corridors.

Growth is currently paying for a lot more than it costs. WE HBA supports the concept that growth should pay for growth, but clearly, new home buyers are being disproportionately targeted for service and infrastructure that benefit all. These taxes cannot be looked at in isolation. Much like cigarettes and alcohol, housing is being treated as a “sin” tax with upwards of a quarter of the price of a new home going to the government through a cumulative sum of different taxes by all three levels of government.

The BILD study asserts that municipalities who maintain large reserve fund balances are impacting housing affordability and falling behind in providing community amenities and infrastructure, like roads, parkland, recreation space and libraries.

Densification could reduce DCs and property taxes

When new housing is built, developers have borne the majority of the initial costs of providing the needed additional service infrastructure through DCs, but the municipal government is responsible for the ongoing operation, maintenance and replacement of this infrastructure, which is paid for in the capital budget by property taxes, provincial grants, and other funding sources.

Once the infrastructure is in the ground, municipalities are forever responsible for operating, maintaining and replacing it. Growing in more compact ways, relying more on intensifying existing urban areas and creating dense, mixed-use new communities can reduce long-term financial commitments and ensure better fiscal health now and for generations to come.

Residential development in urban areas (infill) is more cost efficient than adding new subdivisions

A 2021 report for the City of Ottawa found that to serve new low-density homes built on undeveloped land it costs $465 per capita, per year more than the City receives back in property taxes and water bills, while high-density infill development (eg. apartment buildings) pays for itself and produces a surplus of $606 per capita, per year.

Intensification via development in higher-density urban areas is, on average, the most cost-efficient for the [City of Ottawa], while urban greenfield development and low density rural development are likely costing the City more than is returned in taxes and service rate fees.

A key reason is that urban development is more dense so requires less infrastructure per household. Moreover, urban properties typically have higher real-estate value, so taxes are higher.

Densification reduces per capita costs. It’s way cheaper for a municipal water and sewer system to serve one 200 unit apartment than 200 single family homes. Replacing single family homes with apartments would allow water rates to be decreased even after borrowing money to upgrade infrastructure. The lower the amount of local infrastructure required by new development, the lower the annual replacement costs.

Municipalities don’t always take into account the long-term financial impacts of their growth decisions, contributing to urban sprawl and higher ongoing operating and maintenance costs. This can lead to higher property taxes to pay for existing infrastructure and the justification of higher development charges to pay for future infrastructure.

Denser development drives per capita costs down in a big way:

Much of the cost of water utilities is maintaining the pipes. However, a thicker pipe doesn’t really need more maintenance than a thinner pipe. The driving cost of maintenance is the distance of the pipe. And because single family homes are much more spread out, they cost way more in pipe maintenance.

Utilities can lose up to 33% to 50% of the water to leaks in the water mains. The amount of water leaked is proportional to the amount of pipe in the ground. Denser development means less pipe per person. Which means less water leaked per person. Which means less water supply needed per person.

Energy usage per capita

Road surface and vehicle miles traveled per capita (sprawling suburbs have a lot more road surface than apartment buildings)

Number of fire stations needed to get 15 minute response per capita goes down.

Almost every city service is massively cheaper per capita in dense areas than sparse areas.

If the fees really did exist to pay for the impact of development, the fee schedule would be flipped.

Regulatory timeline

Pre-1980s – Provincial and federal governments paid for infrastructure upgrades.

1989 – DCA introduced in Ontario, allowing municipalities to recover 100% of growth-related capital costs.

1997 – DCA updated to remove eligible services which would have growth-related expenditures, including parkland acquisition, corporate administrative space, arts and entertainment facilities, computer equipment, vehicles and equipment with a useful life of six years or less, and hospitals. This shifted the cost of expansion of these services to existing homeowners.

2015 – Allowed for greater recovery of growth-related transit costs and waste diversion costs, but the provision of landfill sites and services, as well as the provision of facilities and services for the incineration of waste remained ineligible. Further, municipalities were faced with an unfavourable adjustment to the cash-in-lieu for parkland ratio and an inability to collect voluntary payments.

2019 – More Homes, More Choice Act (Bill 108) – List of ineligible services in DCA replaced with list of services eligible for inclusion in a DC bylaw. Exemption for second dwelling units, exclusion of landfills and waste incineration, DCs for rental and non-profit housing could be paid in annual installments over 6 and 21 years, respectively.

2022 – More Homes for Everyone Act (Bill 109) – Requires municipalities to publish the statement of the Treasurer about each Development Charges Reserve Fund, including opening and closing balances of each year, the current year’s distribution of the DC proceeds, any financing transfers and the interest earned on the fund.

Had significant impacts on the way municipalities plan, process and fund development. Changes to the DCA include:

Additional statutory exemptions:

Up to two additional residential units within or ancillary to all new or existing dwellings

Affordable rental/owned units

Attainable unit

Non-profit housing

Inclusionary zoning residential units

Certain residential units in existing rental residential buildings

Removal of “Housing” as an eligible service area

Removal of studies (including the DC background study) as eligible capital costs

Extending the period over which the average historical level of service must be assessed from 10 to 15 years

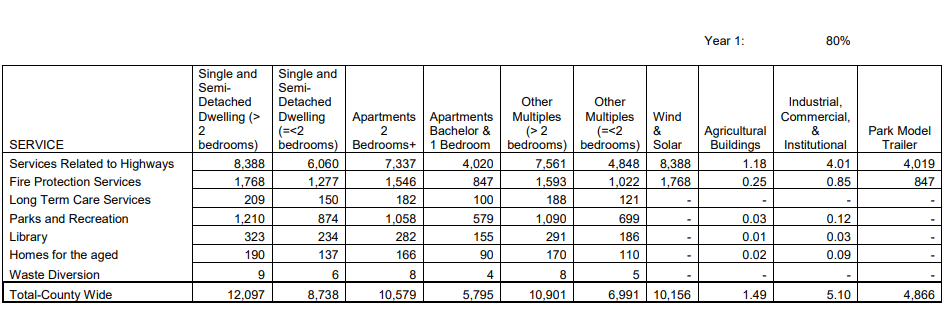

Requiring that all by-laws passed after June 1, 2022 must be phased in relative to the maximum charge over the first five years the by-law is in force, as follows:

Year 1 – 80% of the maximum charge

Year 2 – 85% of the maximum charge

Year 3 – 90% of the maximum charge

Year 4 – 95% of the maximum charge; and

Year 5 to expiry – 100% of the maximum charge

DC by-laws currently expire a maximum of five years after they come into force. This period would be extended to 10 years.

Discounts for rental housing dependent on the number of bedrooms in the units being created

A maximum interest rate would be prescribed at prime plus 1% for the purposes of mandatory installment payments and charges calculated at planning application submission

Requirement to allocate or at least 60% of monies in a reserve fund at the beginning of each year for water, wastewater, and services related to a highway.

Updates the definition of affordable residential unit from 80% of the average market rent/purchase price to the lesser of:

The income-based affordable rent/purchase price for the residential unit set out in the Affordable Residential Units bulletin, as identified by the Minister of Municipal Affairs and Housing in accordance with subsection (5), and

the average market rent/90% of the average purchase price identified for the residential unit set out in the Affordable Residential Units bulletin.

The income-based affordable purchase price applicable to a residential unit is based on:

the income of a household that, in the Minister’s opinion, is at the 60th percentile of gross annual incomes for households in the applicable local municipality; and

the purchase price that, in the Minister’s opinion, would result in annual accommodation costs equal to 30 per cent of the income of the household referred to in clause (a).

However, they have not yet published the Affordable Residential Units bulletin describing the price in each geographic market that would meet the definitions and get the rate cut.

Ontario is giving municipalities more powers to raise dev charges.

April 2024 – Federal government requires 3-year freeze on DCs for municipalities with a population greater than 300,000 to unlock $5B in infrastructure funding

The $5B is for agreements with provinces and territories to support long-term infrastructure priorities through the Canada Housing Infrastructure Fund, part of Budget 2024. Several strings were attached to that funding, including a 3-year freeze on increasing DCs from April 2, 2024 levels for municipalities with a population greater than 300,000.

April 2024 – Cutting Red Tape to Build More Homes Act (Bill 185)

Reduce the time DCs are frozen after complete application or site plan approval from 2 years to 18 months. Failure to obtain a first building permit within that period will result in losing the “frozen” rates.

Comments

We want to hear from you! Share your opinions below and remember to keep it respectful. Please read our Community Guidelines before participating.