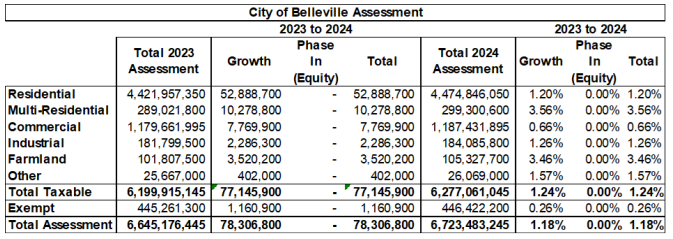

Based on the 2024 returned assessment, the City of Belleville has 21,329 taxable properties with a total value for property taxation purposes of $6.7 billion. Included in this total is $446.4 million in “exempt” assessment which represents 6.64% of total assessment for the City.

Examples of some of the significant exempt properties include but are not limited to Municipal property, Schools, Hospitals, and Churches.

Large commercial property owners filing for property tax relief through the Assessment Review Board

The municipal law as it relates to property taxation continues to be subject to challenge.

In reaction to the effects of the COVID-19 pandemic, some large commercial property owners, ineligible for government relief programs, filed claims for Section 357 tax relief due to the emergent issues created by the pandemic.

While these claims were denied by the Assessment Review Board (ARB), the ruling has been challenged in court. Municipalities across Ontario and the ARB are awaiting decision. The remaining assessment at risk in Belleville is approximately $793M.

As a rough estimate, using the Commercial tax rates for the years in question, an appeal decision rendering an average 25% reduction in the remaining assessment at risk would produce a liability for the City of approximately $6.15M.

As tax appeals commonly take several years to be resolved, the eventual expenditures resulting from current outstanding claims would be determined over years to come. It should be noted that this calculation does not include any potential assessment appeal in 2024 for these properties.

Since 2017, the City has paid out approximately $12.3M in tax adjustments from Assessment Review Board and Request for Reconsideration Appeals, Post Roll Amendments, Amended Notice Adjustments, and Classification changes:

The City has budgeted aggressively for appeals and tax adjustments since 2017, with residual funds being allocated to the Tax Rate Stabilization reserve fund to provide funding availability for assessment at risk. Below is the projected transfer to the Tax Rate Stabilization Reserve fund based on the preliminary 2023 tax adjustments and supplemental taxes:

As the timing of an appeal decision is generally unknown and the magnitude of successful appeals can be significant, it is critical that funding is maintained in the Tax Rate Stabilization Reserve Fund to adequately accommodate against these potential financial risks. For 2023, approximately $2M is projected to be transferred to this reserve fund.

For 2024, a budget of $3.1M is proposed. This funding combined with the reserve fund balance are important to allow the City to fund outstanding and potential appeal settlements in 2024 and beyond.

Supplementary and omitted assessments

Assessment increases that occur after the annual assessment roll has been returned are liable for property taxation. These assessment increases can be supplementary – arising from changes to property values (triggered by building construction), classification, or tax-exempt status – or omissions from the roll when it was returned. Omitted assessments can only be issued for the two preceding tax years.

MPAC is responsible for notifying property owners of any change in property value resulting from a supplementary or omitted assessment. The City issues supplementary/omitted tax bills upon notification by MPAC. A summary of annual supplementary and omitted tax bills is outlined below:

For 2024, staff are proposing a budget for supplementary and omitted taxes of $4.4 million. Over the course of 2022 and 2023 there were significant increases in Building Permit valuations for new construction. At the end of 2023 certain identifiable occupancy permits have been issued supporting significant increases in assessment that has occurred, and should be added to the assessment base in 2024.

The City has benefited from considerable residential growth in recent years. However, continuing commercial tax appeals have and continue to pose a significant cost and financial risk to the City.

Comments

We want to hear from you! Share your opinions below and remember to keep it respectful. Please read our Community Guidelines before participating.